Synthetics: Alternate Realities

There's more than one way to get to your destination

This post is about what I think is the most primary mental model for trading and particularly for derivatives trading: the synthetic position. I’m not going to go into much theory in this post and likely not too much if at all in others. This is meant to be a practical approach. In fact, the source of this blog is a talk I gave years ago when Quantopian was having meet-ups that I called Practical Options Trading (POT). And, yes, well before Elon Musk was posting 42069 all over twitter or X, I thought that was a funny acronym. I like to pride myself on funny blog post titles, but I'm coming up empty this evening.

Before I get into things, a little disclaimer and advice. Everything I’m writing about is for educational purposes only. I will almost certainly make errors and I won’t know ahead of time what they are because, ya know, that’s how errors work. Do Your Own Research (DYOR). Not only will that help with avoiding my inevitable errors, but that will be an education of its own.

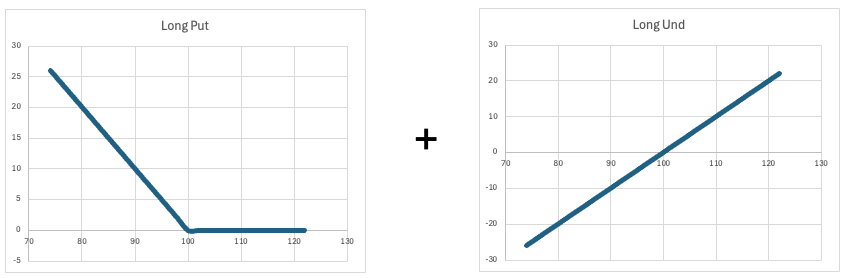

Back to synthetics. The typical example when one reads about synthetics is converting calls into puts or puts into calls by trading underlying against. One can buy a call OR buy a put and buy underlying against it 1:1. From the perspective of payoff, there is no difference between 1) buying the March 2025 CME WTI crude oil (CLH5) $78 call or 2) buying the CLH5 $78 put and 1 CLH5 future. NOTE: I’m pretending that the American exercise does not matter even though it potentially might. NOTE: for stocks, there is the potential for stock related risk due to dividends, takeovers, and perhaps other oddball risks.

All that is done is literally add the profit or loss (pnl) of the long put and long underlying positions. And the resulting chart is identical to the long call. If you have never done so before, I recommend firing up a spreadsheet and replicating the above. This is one type of the DYOR that I mention above.

Perhaps a bit late at this point, I’m going to take a time-out to let you know what my expectations for you are. First, you already know what calls and puts and futures and stocks are. Second, you have some familiarity with expiration diagrams for options. I’ll talk about it, but I’m going to expect you know about the time value of money and how to move cash flows in time. Also that you know what the risk-free rate is and some reasonable knowledge of the US government debt market. If you don’t have all of that knowledge, drop a line in the chat. Based on the response, I can provide resources or a post.

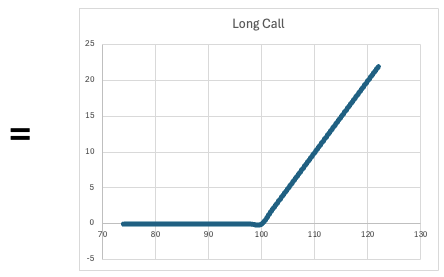

We saw that we can replicate or synthesize a call position by using puts and futures. We can take any of the two in order to make the third. This is what enables put-call parity. Which is another way of saying that if we know the prices of two of these building blocks, then we can figure out the price of the third. It also means that we can offset the original with the synthetic to create an arbitrage. We can 1) buy the call AND 2) sell the put and sell futures to create a conversion. Which, in theory, is now a risk-less position (it is not, but we are not there, yet).

Let’s introduce the cost of money. Here are my building blocks: long call + short put is a synthetic long forward position.

Woo. That brings nothing to the table. Not yet.

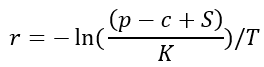

Using the above and the formula from the prior post here:

we can solve for r when we know the relevant prices. We do some algebra to get:

We can go to Nvidia options to check out how market makers are setting “fair value” for the interest rate market makers plug into their option model. For 21-Feb-2025 138 strike: c = 6.6, p = 6.25, S = 137.71 (for trade date 1/17/2025; source Yahoo! finance). Plugging and chugging, we get r = 4.85%. That is a reasonable estimate of the “fair value” discount rate.

What do we mean by fair value? Fair value means the currently perceived median price for an asset. It is often linked to the current mid-market price, but is not strictly mid-market. And the fair value that is at this moment is likely to change, perhaps in the next instant. And it may not be a traded price; it may simply be the price at which price makers aggregate around — meaning there may be different fair values with different traders, but they are all trying to get a sense of a price with an equivalent amount of buying and selling around it.

Why is the risk free rate in the options market not the risk free rate? Theory suggests that the observed discounting rate (the r in the Black-Scholes-Merton formula) should be something like the corresponding US Treasury’s market yield, e.g., 3-month T-bills. It is not because aggregated market participants don’t get funded at the same rate as the US government. Let’s take a step back for a moment. Suppose that a market maker thought that the rate should be 4.25%. That would drop the price of calls, raise the price of puts (dropping calls by 4c and raising puts by 4c). The market maker would be consistently selling calls, buying puts, and to hedge that, buying NVDA stock. The NVDA stock has to be paid for and market makers have to borrow the money to pay for it. If that rate is 4.25% or less, then our market maker friend is fine. If the rate turns out to be 5.00%, the market maker will lose 75bps until he adjust his rate to a level that balances out his stock purchases and sales. Right now, that level is 4.85%. Tomorrow it may be 4.5% and next week 5% (this is called “rho” risk).

Similarly, had the market maker set rate parameters too high, e.g., 5%, and thereby made the operation the best bid for calls, best offer for puts. That would result in purchasing calls, selling puts, and hedging by selling stock. Selling stock raises money in the trading account. If the account earns only 4.5%, then there would be a 50bps loss in the account over the course of time.

This is all cash flow math. In the first case, the market maker lent money up front at 4.25% (buying the 138 strike at 137.73 to collect 27c — call price 6.56 and put price 6.29 for a difference of 27c). Then had to borrow it back from the prime broker / clearing firm at 5% which cost 5% * 138 * 35 / 365 = $0.66 (yes I could have used continuous compounding but this is close enough and, perhaps, a little easier to see/understand). Bad trade.

Great. Where am I going with this? 4.85% might be fair value to the market maker in order to balance lending and borrowing for their firm. YOU can take advantage of that. Originally, when I wrote about the call being 6.6 and the put 6.25, that is not exactly true. That was the mid-market pricing. The call market was 6.55-6.65 and the put market was 6.2-6.3. That means that the NVDA 21-Feb-2025 market on lending & borrowing USD was 4.1% - 5.61%. And that is, of course, not counting any fees to trade. So how is this helpful?

Goal is to get long NVDA stock and there is no readily available cash. Your broker’s margin rate is 11% to borrow USD to buy the stock. Instead, you buy call, sell put to purchase the synthetic stock position paying 5.61% financing.

Goal is to purchase an NVDA call, you have excess cash in your portfolio. Your broker’s sweep account pays 2%. NOTE: this is not really the case right now but during the era of 0% Fed target rate, this was pretty normal. Plugging in your rate of return (2%) values the call 6.41 and put 6.44 — in this case making the purchase of the put with stock the better value specific to YOU.

You are limited in short term investments. Perhaps your brokerage sweep account only earns 2%. Then you could sell call, buy put, and buy stock to earn 4.1%.

NOTE: these are not risk-free! They are not fee-free! The goal here is to break you out of the rut of thinking that fair value applies the same way to everyone. It does not! This sort of thing is fun, has potential, and takes work. One has to be aware of dividend payouts, mergers and acquisitions, early exercise, and potentially other impacts. The naive positive carry investment is most easily carried out where the contracts are simplest, e.g., European exercise style and not single name stocks. DYOR, DYOR, DYOR.

NOTE: For those who know options, I’ve been playing a little loose on parameters & pricing, i.e., r - risk free rate and b - cost of carry. The points are still valid.

Thanks for the post, you mentioned that you could give some resources to help with the fundamental knowledge required to follow. I vote +1 on that!

Thank you for the post!